It's okay to look away

A few curious professors decided to run an experiment. The fact that two of them later became Nobel Prize winners… well, that probably has a bit to do with the outcome.

The experiment was simple. They told volunteer students that they were the portfolio manager of the Berkeley Endowment and they had two investment options. The first was riskier but had higher returns. The other was a safer investment option with lower returns. The students could initially select and then modify their portfolio allocation between the two investment choices.

So, what exactly was the purpose of the experiment?

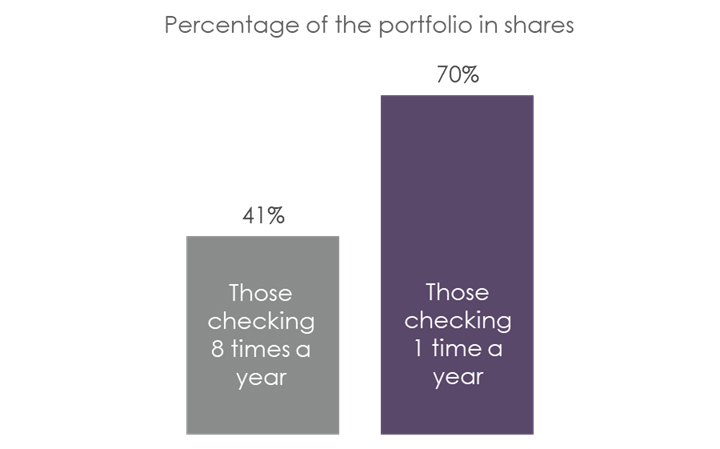

The portfolios provided to the students were identical. But the professors also controlled how often their subjects could look at the performance of their investments. One group of students were allowed to check their investment performance eight times per year. The other group was only allowed to view the performance once a year.

What the professors hoped to find out was - does the frequency that you look at the performance of a portfolio change the type of asset allocation you think is best?

Those checking performance eight times a year allocated 41% of their portfolio to shares, on average.

Those checking performance once a year allocated 70% of their portfolio to shares, on average.

In other words, the frequency with which you looked at the results fundamentally changed your portfolio preference.

Recently, another professor replicated the study with a twist. In a 14 day trial, the professor gave one group of students continuous access to returns information on their portfolio. He gave a second group information on price changes only every four hours. Both groups were trading an investment with the exact same price movements. The only difference was the frequency the two groups saw those price movements.

The professor also made it a high stakes contest, so the students were all motivated to do well.

Over the 14 day experiment the professor found, those with less frequent price information invested 33% more in shares and earned on average 53% higher profits.

The conclusions here are fascinating. Both studies seem to suggest that the more information you have about the price movements of your portfolio, the worse your results. That feels counter intuitive. Shouldn’t it be that access to more information helps us to be better and smarter?

Well, not when that information is infused with emotion. What the studies demonstrate is something academics call “Myopic Loss Aversion”. Most of us would simply describe this as “not happy to see losses in my portfolio.”

The way the professors describe the reaction, is that losses feel bad approximately twice as much as gains feel good. We probably know that intuitively. I know that because my kids just played paper, scissors, rock and the loser was grumpy for 30 minutes while the winner moved on to the next thing in 30 seconds. Losing feels worse than winning feels good.

But what does that have to do with frequency of seeing portfolio returns? As it turns out, everything. If you look at a portfolio often you are more likely to see a loss. On a daily basis, a share portfolio will be up only about 51% of the time. But if we look on an annual basis, a share portfolio tends to be up about 81% of the time (3).

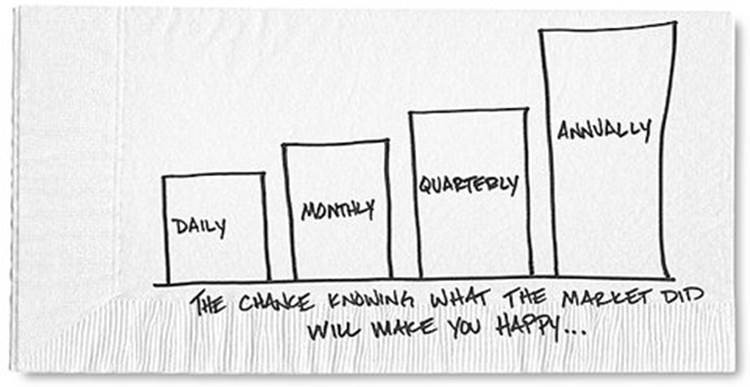

Carl Richards, author of The Behavior Gap puts it more simply in a drawing he titled “The chance knowing what the market did will make you happy.”

Why is this important? Well, if you are comfortable with disappointment, feel free to check the value of your portfolio as frequently as humanly possible. For everyone else, it is a studied fact that the less frequently you check your portfolio the happier you are likely to be. Checking too often can also tempt some investors into abandoning a well-conceived plan simply on the basis that it momentarily doesn’t feel good.

What’s the bottom-line? After wide ranging studies and intensive analysis, some of the most highly credentialled behavioural economists in the world distilled a simple guiding principle for you and your portfolio… don’t look at it!

Or, to put it another way, it’s okay to look away. If you do, you are likely to be a much happier and more successful investor as a result.

Ben Brinkerhoff

Head of Adviser Services, Consilium

-

Resist the itch to switch

Day after day we are bombarded by the media and at the moment, we are seeing nothing but bad news. Coverage of the share market is full of headlines with words such as “plunge”, “recession” and “loss” repeated over and over again.

-

Business will never go out of business

Benjamin Roth was a lawyer in Youngstown, Ohio, when the stock market crashed in 1929. Two years later he decided to keep a diary to detail the effects that the financial collapse had on himself, his neighbours, and the nation. Mr. Roth kept his diary for ten years. In the late 1930s, when the depression had mostly passed, he summarised a few points he had learned from the experience.

-

Avoid the prediction addiction

1968 was a great year. New Zealand won a gold in rowing at the Mexico Olympics, The Beatles recorded "Hey Jude", the United States at long last passed the Civil Rights Act and an expert biologist at Stanford predicted the end of humanity.