Quarterly market commentary - June 2024

Positive global share market momentum carried into the second quarter of 2024 for the USA, while share market returns in other regions were variable.

The outlook for interest rates remained unchanged, however there is growing expectation for a general reduction in interest rates around the globe. In June, the European Central Bank and the Bank of Canada became the first of the major banks to begin cutting rates. With local inflation heading in the right direction, it looks as though the Reserve Bank of New Zealand may soon follow suit.

In the key US market, the Federal Reserve held the federal funds rate steady at 5.25% throughout the quarter, with officials there citing the need to cool persistently high inflation.

Against this backdrop, the US share market extended its bull run that began in late 2022, with the S&P 500 Index reaching all-time highs during the quarter. This performance was led, once again, by the strong performance from a handful of large capitalisation companies in the information technology sector. Unfortunately, the New Zealand share market continues to lag many of its global peers with weak economic growth, and stubborn inflationary pressures, continuing to challenge local policymakers.

On the global political stage, uncertainty and change seem to be in store in 2024. After a relatively brief campaign, the Conservatives have just relinquished Downing Street after 14 years in power in the UK. Emmanuel Macron’s snap election resulted in no clear winner, leaving France without a new prime minister or government and in political chaos just weeks before they welcome the world for the Olympic Games. Meanwhile, the lead-up to the US presidential election has been even more volatile than pundits expected, including the shocking attack on former president Donald Trump in early July and the recent exit of Joe Biden from the Democratic ticket.

New Zealand interest rates - the wait goes on

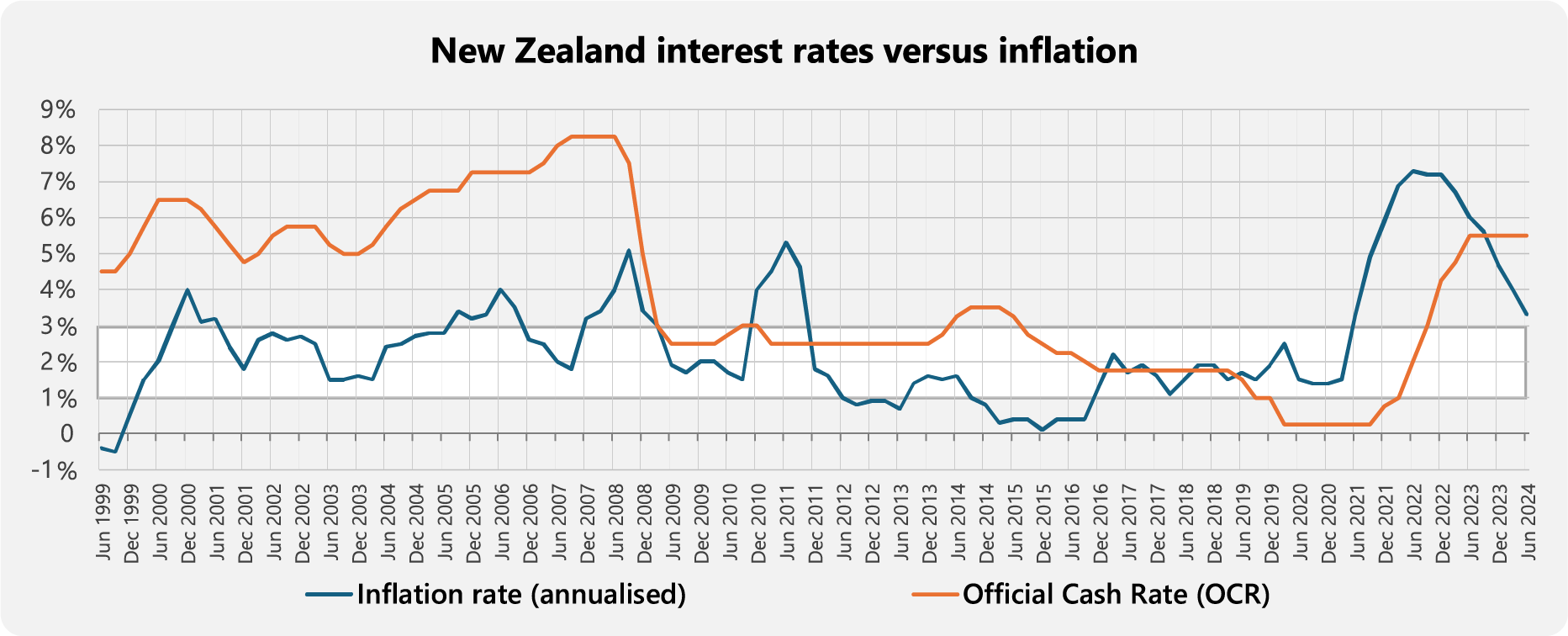

The chart below shows the annualised inflation rate (dotted blue line) plotted against New Zealand’s Official Cash Rate (OCR) which is the short-term interest rate set on a periodic basis by the RBNZ (orange line).

The RBNZ aims to keep inflation within the range of 1% to 3% over the medium term (the area shaded in white). For the most part they have achieved this fairly consistently over the last 25 years. Up until 2021, there had been only occasional deviations of inflation outside this band, and most had returned back to the target range within 12 months.

However, the 'cost-of-living crisis' has been a different story. The significant ‘spike’ in inflation that commenced in 2021 has so far not returned to the target band. This is why the orange line is not budging yet. The length of time that inflation has stayed above target (now three years and counting) has backed the RBNZ into a corner. It is highly reluctant to reduce interest rates until it sees inflation back inside the target band. This caution has resulted in the OCR being stuck at 5.5% since May 2023.

The good news, as you can see from the chart, is that inflation is heading in the right direction, and many commentators consider that we could see interest rate reductions later this year (ahead of the RBNZ’s own forecasts). Whenever it begins, it will mark the end of the most restrictive interest rate settings New Zealand has experienced in 15 years.

Does the US election matter?

We are approaching a pivotal moment in the U.S. political landscape, as President Joe Biden has officially announced that he will not seek re-election. This decision significantly alters the upcoming election, which is now likely to feature former President Donald Trump as the presumptive Republican nominee. Trump is known for being a divisive and controversial figure, and his campaign is expected to involve considerable time in courtrooms as well as on the campaign trail. He will face off against a yet-to-be-confirmed Democratic candidate, with Kamala Harris seemingly the frontrunner.

Does it matter who wins?

In some ways, probably not. Both the Democrats and Republicans will aim to be expansionary and will keep issuing bonds and printing money. While the Democrats might spend more, the Republicans will aim to reduce taxes more.

In some ways, almost certainly. In matters of foreign policy, we can expect a Republican presidency to renew stronger rhetoric around Europe’s contributions to NATO, possibly not supporting efforts to arm Ukraine, and likely promoting greater trade protectionism, particularly in respect to China. Conversely, the Democrats have indicated they will propose extending tax breaks for those on low incomes while raising corporate tax rates, and potentially further promote renewable energy development. Clearly the outcome in November will have a significant impact on some sensitive corners of the economy.

How investment markets might perform is much less predictable, although history says that patient investors will be rewarded regardless of which political party controls the White House.

One of the reasons why is because the president has no direct control over the share market. While the president influences fiscal policy to varying degrees, it is Congress that ultimately creates the federal budget, and government spending is only one of many variables that affect the share market. Also, when considering events like the dot-com bubble, the Great Recession, and the COVID-19 pandemic - no president caused those events, but all three events caused share market crashes.

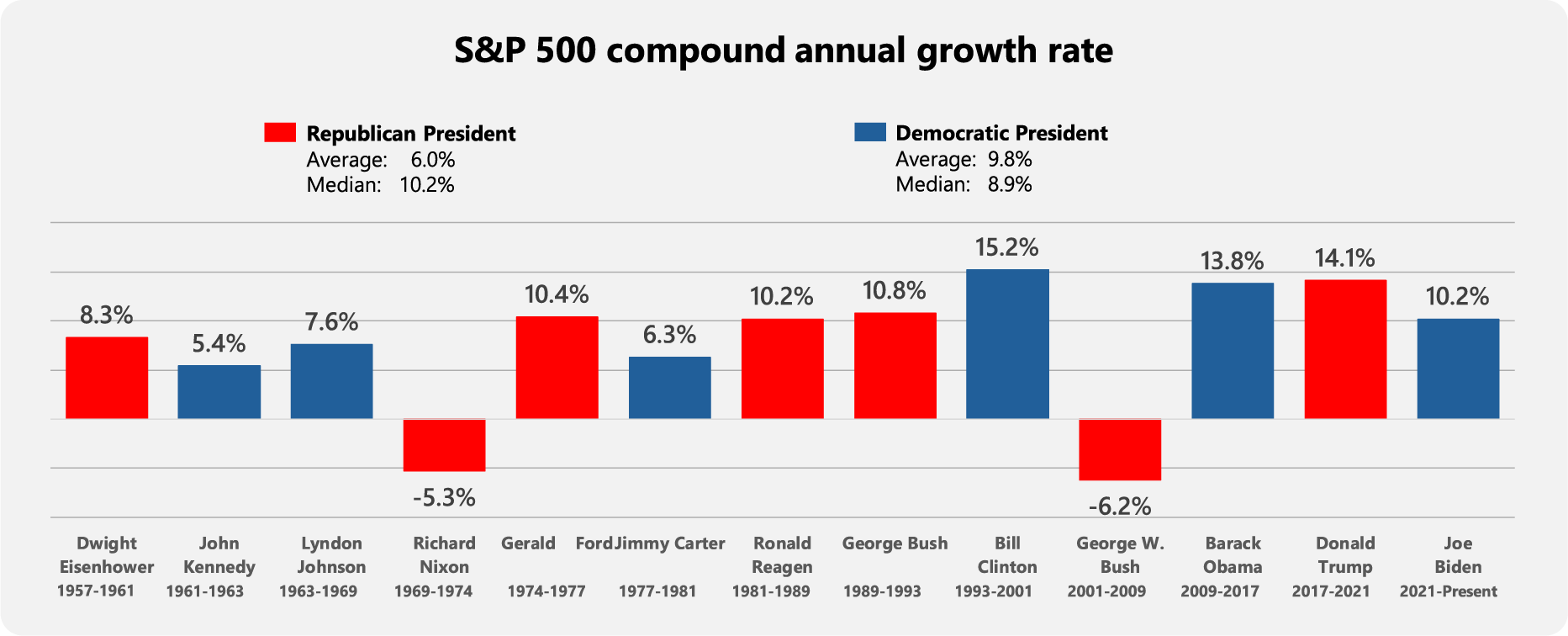

Since the inception of the S&P 500 share market index in 1957, the respective market performance under different presidencies is highlighted below.

Given the ability for statistics to be easily manipulated, Republicans (higher median return) and Democrats (higher average return) could both try to claim the share market has performed better when they controlled the presidency.

However, investors should ignore such comments. Share prices, determined by business fundamentals like revenue and earnings growth, are merely influenced (not controlled) by a president’s fiscal policies.

While the winner in November may not have much of an impact on eventual market returns, this will nevertheless be a point of considerable global attention over the next 4-5 months.

Tune out the noise

There is a near constant swirl of speculative opinion - both in the general news media and in the financial press - about a range of factors or events for which the outcome is, and always will be, uncertain.

Not a day goes by without a big, scary headline professing at least some level of consternation about one or more of the following:

- the timing and size of future interest rate changes

- the long-term impact of AI

- the consequences of a changing global political landscape

- whether inflation is really back under control

- whether technology companies are forming the next market ‘bubble’

- when the conflict in Ukraine or the Middle East might end

- the ongoing impacts of climate change

Unfortunately, reading (or watching) the guesses of different pundits about an unknown future provides no useful benefit to long term investors.

Markets, in aggregate, are aware of the prevailing uncertainties and, to the greatest extent possible, that uncertainty is already factored into asset prices today. Yes, as information changes, prices will move to reflect that new information. But, as the exact nature of future information is usually unguessable in advance – even by so-called experts – this speculation is nothing more than an unwelcome distraction and investors should exclude it from their strategic decision-making.

The best response a long-term investor can have to uncertain events is to tune out the persistent noise about everything that is unknown or could go wrong and focus instead on the consistent behaviours that have been proven to add value over time.

Unlike the list of potential issues, which is always concerning and always changing, the list of great investor behaviours never changes.

These are – in no particular order:

☑️ allocate strategically (not tactically),

☑️ keep costs low, stay diversified, rebalance periodically to manage risk,

☑️ don’t engage in panic buying (or selling),

☑️ and always consult your adviser if your circumstances or requirements change.

Mastery of these relatively simple steps means you will dramatically improve your chances of achieving your long-term investment goals and objectives.

For a detailed review of the asset class performances for the quarter, see ‘Key market movements - June 2024’

Click here to view the full newsletter in PDF

Disclaimer

While every care has been taken in the preparation of this newsletter, Consilium makes no representation or warranty as to the accuracy or completeness of the information contained in it and does not accept any liability for reliance on it. Information contained in this newsletter does not constitute personalised financial advice and does not take into account your individual circumstances or objectives.

-

Key market movements - June 2024

International share markets gained overall in the second quarter of 2024, although individual country returns were mixed. Politics was a key focus for the quarter. Outside of this, the artificial intelligence “theme” continued to lead markets, while policymakers continued to wrestle with how much (and when) to reduce interest rates.

-

Habits vs. Goals: A Look at the Benefits of a Systematic Approach to Life

Nothing will change your future trajectory like your habits. Habits are algorithms operating in the background that power our lives. Good habits help us reach our goals more effectively and efficiently. Bad ones make things harder or prevent success entirely. Habits powerfully influence our automatic behavior.

-

Quarterly market commentary - March 2024

Diversified investors had more reasons to smile as the markets began this year exactly as they left off last year - with another strong gain by most international share markets. In the absence of any major new economic or geopolitical shocks, investment sentiment continued to be closely linked to changes in the inflation and interest rate landscape. On that front, the first quarter of 2024 saw another discernible shift in inflation and interest rate expectations.