Quarterly market commentary - September 2023

In some welcome news, the world economy is showing signs of resilience this year despite lingering inflation and a sluggish recovery in China. The International Monetary Fund (IMF) released its latest World Economic Outlook in July, where they noted this resilience is increasing the odds that a global recession may be avoided.

The outlook was rosier in large part because financial markets - which had been shaken by the collapse of several large banks in the United States and Europe earlier in the year - have largely stabilised.

Sadly, in early October, Palestinian militant groups led by Hamas launched a large-scale invasion against Israel from the Gaza Strip, triggering a swift response from the Israeli military. While geo-political conflict tends not to directly impact markets, all independent observers will be hoping for a speedy resolution.

Key commodity prices weaken

Weakening trading partner demand, driven by the slowing Chinese economy, has resulted in a significant decline in New Zealand's commodity export prices in recent months, none more so than in the dairy sector.

In early August, Fonterra reduced its 2023/24 season milk price forecast by one dollar to a mid-point of $7 per kg of milk solids. This was a mid-point forecast and was subsequently raised to $7.25 on 9 October, still far below last year's payout. Given the sheer volume of milk solids that Fonterra collects each year, this forecast reduction equates to around 0.4% of New Zealand’s gross domestic product (GDP) before any indirect economic effects are considered. Some economists suggest the total impact on the economy could be as much as 4 to 5 times the direct effect.

The forecast price of $7.25 per kg of milk solids is 12% lower than last season’s price and also below most estimates of a breakeven rate. This is noteworthy because dairy is our largest export, making up almost a third of New Zealand’s total goods exports.

Other key export prices for lambs and logs have also been under pressure from slowing demand. Unfortunately, while prices have been weakening, farm costs have been moving in the other direction, increasing the pressure on our agricultural sector.

As lower prices generally mean lower export revenues, this is likely to lead to at least a temporary reduction in New Zealand’s overall economic activity.

Housing decline over?

On the flip side, the local housing market has finally shown some positive signs of stabilising.

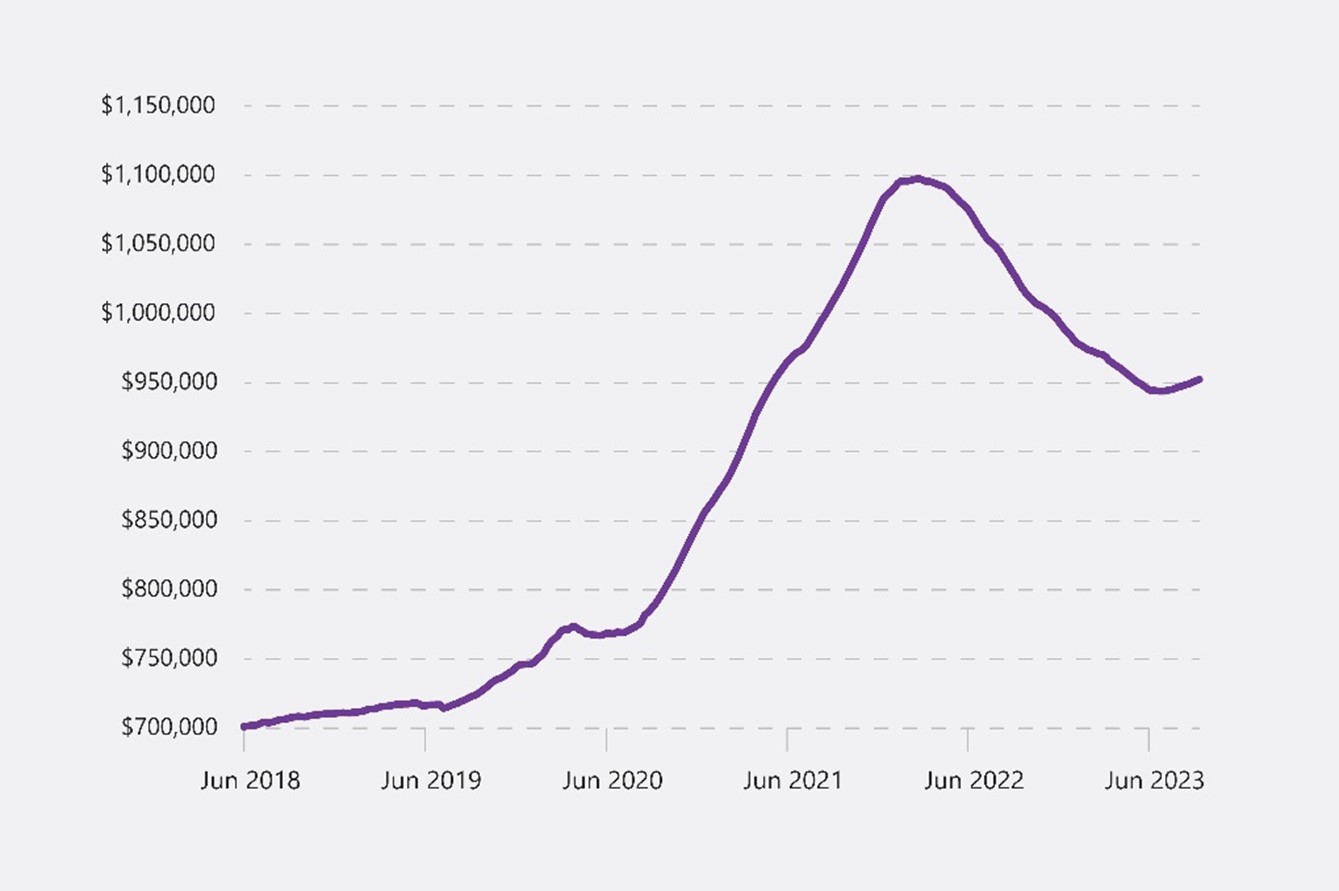

Figure 1: New Zealand’s average property value since June 2018

Source: Property value data derived from the OneRoof-Valocity House Value Index, taken on 20 September, 2023.

From August 2020 to February 2022, with our international borders still closed, and as the New Zealand economy reoriented itself after the national Covid lockdown, the average value of the local housing market increased by just over 40% in 18 months.

This turned around over the following 16 months to June 2023 as New Zealanders finally got their boarding passes again, mortgage interest rates began to rise quickly and inward migration flows remained frustratingly weak.

Today, with inward migration numbers very much higher again (adding further weight to housing demand) and interest rates having stabilised, housing values have slowly begun to pick up again. For many who have their total net worth closely linked to the value of their home, this has been a ray of sunshine in an otherwise challenging economic environment.

Interest rates stabilised

The Reserve Bank of New Zealand (RBNZ) continues to believe it has done enough to get inflation back under control. Across the 12 July, 16 August and 4 October monetary policy decisions, the RBNZ left the Official Cash Rate (OCR) unchanged at 5.50% and made only very small changes to its forward-looking OCR forecast. This demonstrates a degree of confidence within the RBNZ that, even with current inflation still elevated, it remains on track to achieving its inflation target.

The RBNZ believes the current level of interest rates is limiting spending and reducing inflation pressures and headline inflation is tracking downward. This has been largely driven by a useful fall in the price changes for goods and services that are more exposed to international competition. Unfortunately, inflation on the domestic goods and services we use daily such as construction, rents, restaurant meals and ready-to-eat food is reducing much more slowly.

Inflation in domestic goods and services is proving to be a bit ‘stickier’ than the RBNZ originally hoped, however, there is an emerging consensus that overall inflation is at least heading in the right direction. A number of commentators are suggesting this could lead to reductions in the OCR from early next year, even though the RBNZ’s own forecasts suggest this might not happen until 2025.

Diversification remains valuable

Since the emergence of Covid-19 back in early 2020, global asset markets have generally experienced some degree of upheaval. At the beginning of the pandemic, global share markets capitulated over the first few weeks of March 2020 before embarking on a searing rally. In the case of the New Zealand NZX 50 Index, this rally was so strong that by September 2020, it had recovered all of its lost ground from earlier in the year.

So, what has happened in the three years since then?

As the table below shows, it’s been a relatively underwhelming period for New Zealand shares, with the local index (including dividends) having ground out a small annualised loss for the period. With the benefit of hindsight, that’s not a shocking discovery. The small New Zealand economy was slower to reopen to the rest of the world. It has since been on the back foot trying to compete for much-needed skilled labour, in what has suddenly appeared to be a global labour market shortage.

For investors with all their growth assets in New Zealand, that wouldn’t have been a great result, but for diversified global investors the story has probably been more positive.

| Main share market index returns | Currency | 3 years to end Sept 2023 (p.a.) |

| S&P/NZX 50 Index (gross with imputation credits) | NZD | -0.50% |

| S&P/ASX 200 Index (Total return) | AUD | 11.00% |

| S&P/500 Index (Total return) | USD | 10.15% |

| MSCI Emerging Markets Index (Gross div.) | USD | -1.34% |

The neighbouring Australian share market (ASX 200) and the globally significant US share market (S&P 500) both delivered excellent returns over the same three year period, rewarding investors who were mindful not to have all their growth exposures in New Zealand.

Outside of global shares, a number of other asset classes also struggled.

| Other notable index returns | Currency | 3 years to end Sept 2023 (p.a.) |

| S&P/NZX A-Grade Corporate Bond Index | NZD | -2.79% |

| Bloomberg Global Aggregate Bond Index (Hedged to NZD) |

NZD | -3.93% |

| S&P Developed Property Index (Total return) | USD | 1.47% |

| S&P/GSCI Gold Index (Total return) | USD | -1.38% |

Bond markets in New Zealand (A-Grade Corporate Bond index) and internationally (Bloomberg Global Aggregate Bond index) all laboured as global interest rates generally rose. Importantly, higher interest rates now mean higher expected returns from bonds in the future.

Global listed property produced a weak positive three year return, while gold – often touted as a safe haven in times of market trouble – could only deliver a small negative return.

While Bitcoin did very well (initially), its highly speculative properties make it an unsuitable holding for most investors, something which its price decline of -60% since October 2021 probably confirms.

If in doubt, stick to the plan

With international inflation pressures slowly receding and the outlook for global growth looking slightly brighter, investors can take a little bit of heart.

The last few years have been a period unlike any we’ve experienced previously, with the global economy effectively shutting down for a period of time and no rule book on how to get it successfully restarted. Perhaps not surprisingly, the economic transition back from the depths of the pandemic has been far from painless.

In New Zealand alone over the last three years, we’ve witnessed rampant house prices (followed by rapidly falling house prices), galloping inflation, a cost-of-living crisis and extreme labour shortages. We have, however, endured. And well diversified investment portfolios have endured as well – particularly those containing at least a scattering of traditional international growth exposures.

To the layperson, investing through the 'good times' is often considered easy – when just having your money somewhere will end up giving you a good return. However, it’s when navigating the 'difficult times', that a robust strategy and good investor behaviour will often pay the biggest dividends. That doesn’t necessarily mean earning higher returns, but it almost always means helping investors avoid the pitfalls of succumbing to short term (emotionally driven) thinking and bad decision-making. Doing the wrong thing at the wrong time is the surest way we know to undermine even the smartest strategy.

The challenge is that no matter how obvious everything seems in hindsight (once events have happened and their consequences are known), it’s usually impossible to know which period – good or bad – lies immediately ahead. All we have is the certainty that both will make an appearance at different times and, on average, there will be more good than bad.

That’s why adopting a sound long term investment strategy is so important; one that allows someone to stay invested when the going gets tough, so they are in the best position to benefit from the inevitable recovery.

For a detailed review of the asset class performances for the quarter, see ‘Key market movements - September 2023’

Click here to view the full newsletter in PDF

Disclaimer

While every care has been taken in the preparation of this newsletter, Consilium makes no representation or warranty as to the accuracy or completeness of the information contained in it and does not accept any liability for reliance on it. Information contained in this newsletter does not constitute personalised financial advice and does not take into account your individual circumstances or objectives.

-

Key market movements - September 2023

After a generally good performance over the first half of 2023, international share markets gave up some of their gains in the July to September quarter.

-

Your happiest time in life is still ahead of you — way ahead of you

If you thought the carefree days of your youth were behind you, or that happiness was a thing for the young, have we got a surprise for you. Scientists from Germany and Switzerland recently pinpointed the age at which people are happiest, and it’s not your twenties. Or your thirties. Or your forties. Or even your fifties. Or even...you get the point.

-

Quarterly market commentary - June 2023

As the grey clouds gather for winter, it's pleasing to report the sun is still shining on portfolios. With New Zealand in a technical recession, there are signs that short-term interest rates could begin falling again in 2024.